Executive Summary: The Year Silver Broke Free

Key Takeaways

•A Historic Repricing: 2025 was the year silver broke free, posting gains of over 140% and hitting an all-time high of ~$84, driven by physical scarcity rather than paper speculation.

•The Inventory Shortage: A cumulative 1-billion-ounce deficit since 2019 has drained global vaults. Physical shortages in Shanghai and London are now dictating global spot prices.

•Strategic Shift: Silver is no longer just a currency hedge; it is a strategic industrial asset. China's new export controls and the US "Critical Mineral" designation have turned the supply chain into a geopolitical battleground.

•The New Floor: The structural squeeze suggests the days of sub-$30 silver are over. $50 per ounce has emerged as the new psychological and physical floor for 2026.

•Industrial Demand is Key: Inelastic demand from Solar PV, EVs, and AI hardware is overwhelming flat mine supply, creating a long-term bullish case despite short-term volatility.

The financial year of 2025 will undoubtedly be recorded in economic history as a watershed moment for the global silver market, marking the definitive decoupling of the metal from its traditional tether to gold and speculative paper derivatives to be repriced as a critical strategic industrial asset.

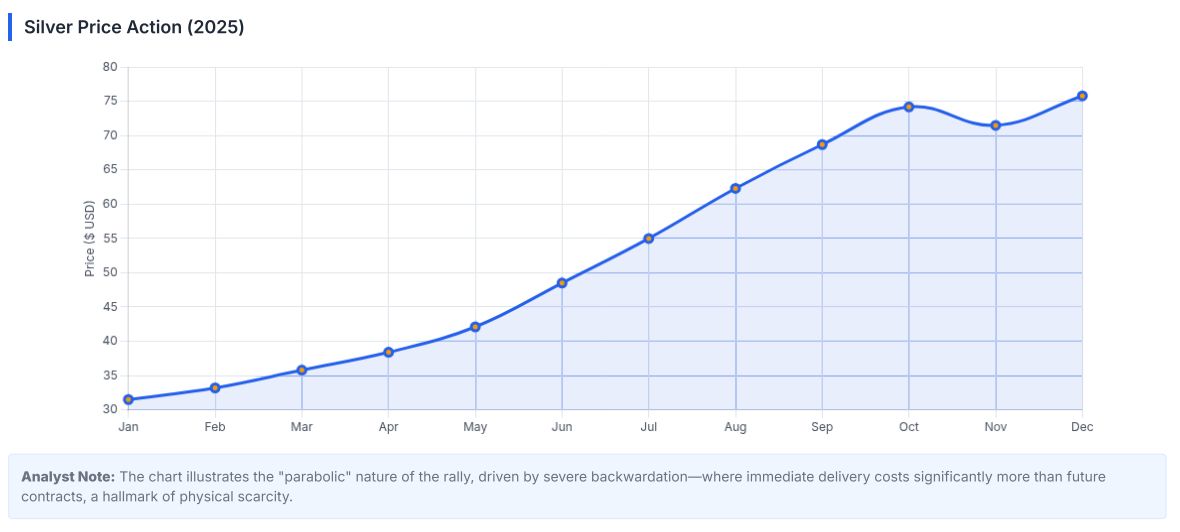

After decades of trading in the shadow of its monetary cousin and being subject to the caprices of high-frequency trading algorithms, silver staged a parabolic breakout in the fourth quarter that fundamentally altered its valuation model. This culminated in the historic "Christmas Rally" of December 2025, a period of extreme volatility and price discovery that saw silver briefly shatter the $80 per ounce ceiling before regulatory intervention precipitated a sharp correction.

This comprehensive research report, produced specifically for the Silver RWA community, provides an exhaustive supply and demand analysis of this transformative year. We aim to dissect the mechanics of the market movements, moving beyond superficial headlines to understand the deep structural currents that drove prices to record highs.

The evidence gathered from global exchanges, mining reports, and geopolitical developments suggests that the 2025 rally was not a fleeting speculative bubble, but rather the violent resolution of a seven-year structural deficit that had been building largely unnoticed by the mainstream financial press.

By December 2025, the cumulative supply shortfall since 2019 had exceeded 1 billion ounces, effectively draining above-ground liquidity to critically low levels across the world's major trading hubs.[1] For the first time in the modern era, pricing power began to shift aggressively from the derivatives markets of the West—specifically the COMEX in New York and the LBMA in London—to the physical delivery centers of the East, most notably the Shanghai Gold Exchange (SGE) and the Shanghai Futures Exchange (SHFE). This geographic arbitrage, driven by China's insatiable industrial appetite, forced a reckoning in global spot prices.

The catalysts for this repricing were manifold and mutually reinforcing. They included a classic "gamma squeeze" in the options market that forced market makers to chase price action; unprecedented and inelastic industrial demand from the burgeoning solar photovoltaic and Artificial Intelligence sectors; and a decisive geopolitical pivot by the People's Republic of China to classify silver as a restricted strategic resource, instituting strict export controls that shocked global supply chains.

[3] While regulatory interventions in the form of aggressive CME margin hikes triggered the so-called "Christmas Crash," the market structure has been irrevocably altered. With global inventories at multi-year lows and mine supply structurally inelastic due to geological constraints, $50 per ounce has emerged as the new psychological and physical floor for the metal.[1]

This report offers retail investors and industry observers a granular, data-driven understanding of why the "poor man's gold" has evolved into the world's most critical strategic metal, detailing the supply chain vulnerabilities, the demand shocks, and the future outlook for 2026.

1. The 2025 Market Landscape: A Year of Records and Ruptures

1.1 The Quantitative Breakout and Asset Class Outperformance

Silver delivered one of the most explosive performances in the history of commodities during 2025, posting annual gains that exceeded 140% by the close of the year.[1] To contextualize the magnitude of this move, it is necessary to compare it against other major asset classes.

While gold, the traditional safe-haven asset, posted a robust and historically significant gain of roughly 65-70% driven by central bank buying, silver's performance was more than double that of its yellow counterpart.[6] Furthermore, silver absolutely crushed the broader equity markets; the S&P 500, despite a strong year driven by the AI narrative, posted a gain of roughly 16%.[8]

This performance gap highlights a critical theme of 2025: the return of the "beta" trade, where silver acts as a high-octane version of gold, but also the emergence of an "alpha" trade, where silver moves independently based on its own idiosyncratic fundamentals.

For years, the Gold-to-Silver Ratio (GSR)—a key metric used by precious metals investors to determine the relative value of the two metals—hovered stubbornly near 80:1 or even 100:1. This signaled a profound historical undervaluation of silver. By late December 2025, however, this ratio had collapsed to approximately 57:1.[6] This compression was not merely a statistical mean reversion; it was a market signal that silver was being priced for its industrial utility and scarcity rather than just its precious metal correlation.

The climax of the year occurred in December. Following a decisive technical breakout above the $50 multi-year resistance level in October—a level that had capped prices since the 1980 Hunt Brothers squeeze and the 2011 peak—prices went parabolic. On Sunday, December 28, amidst thin holiday trading, silver futures spiked to an intraday all-time high of approximately $84.00 per ounce.[6] This move shattered the previous nominal record of $49.45, psychologically liberating the market from forty-five years of resistance.[11]

1.2 The "Christmas Rally" Phenomenon: Anatomy of a Squeeze

The "Christmas Rally" of 2025 was driven by a perfect storm of low liquidity, high anxiety, and relentless physical accumulation. Historically, the "Santa Claus Rally" refers to a seasonal tendency for equities to rise in the final week of December due to tax considerations and optimism for the new year. In 2025, however, this liquidity vacuum was weaponized in the precious metals market to trigger a massive squeeze.

As Western trading desks went skeleton-staffed for the holiday season, physical buyers in Asia continued to bid aggressively. The divergence between paper prices (futures) and physical reality became undeniable. While Western paper markets were often closed or thinly traded, physical premiums on the Shanghai Gold Exchange (SGE) exploded, trading at double-digit dollar premiums over the theoretical COMEX price.[9] This arbitrage window incentivized a massive movement of physical metal from West to East, further tightening the Atlantic markets.

However, this rally was met with a brutal counter-attack from market regulators. On December 29 and 30, the CME Group, operator of the COMEX, implemented aggressive margin hikes to curb the exploding volatility.[13][14] By significantly raising the capital requirements ("initial margin") required to hold silver contracts, the exchange forced leveraged speculators to liquidate their positions or face default.

The resulting "Christmas Crash" saw silver plunge nearly 10-14% in single trading sessions, pulling prices back to the $70 range by year-end.[15] Despite this volatility, the year-end close represented a paradigm shift, solidifying the metal's valuation in a completely new tier and leaving the sub-$30 prices of the past as a distant memory.

2. The Supply Crisis: Seven Years of Structural Deficits

2.1 The Cumulative Deficit Analysis

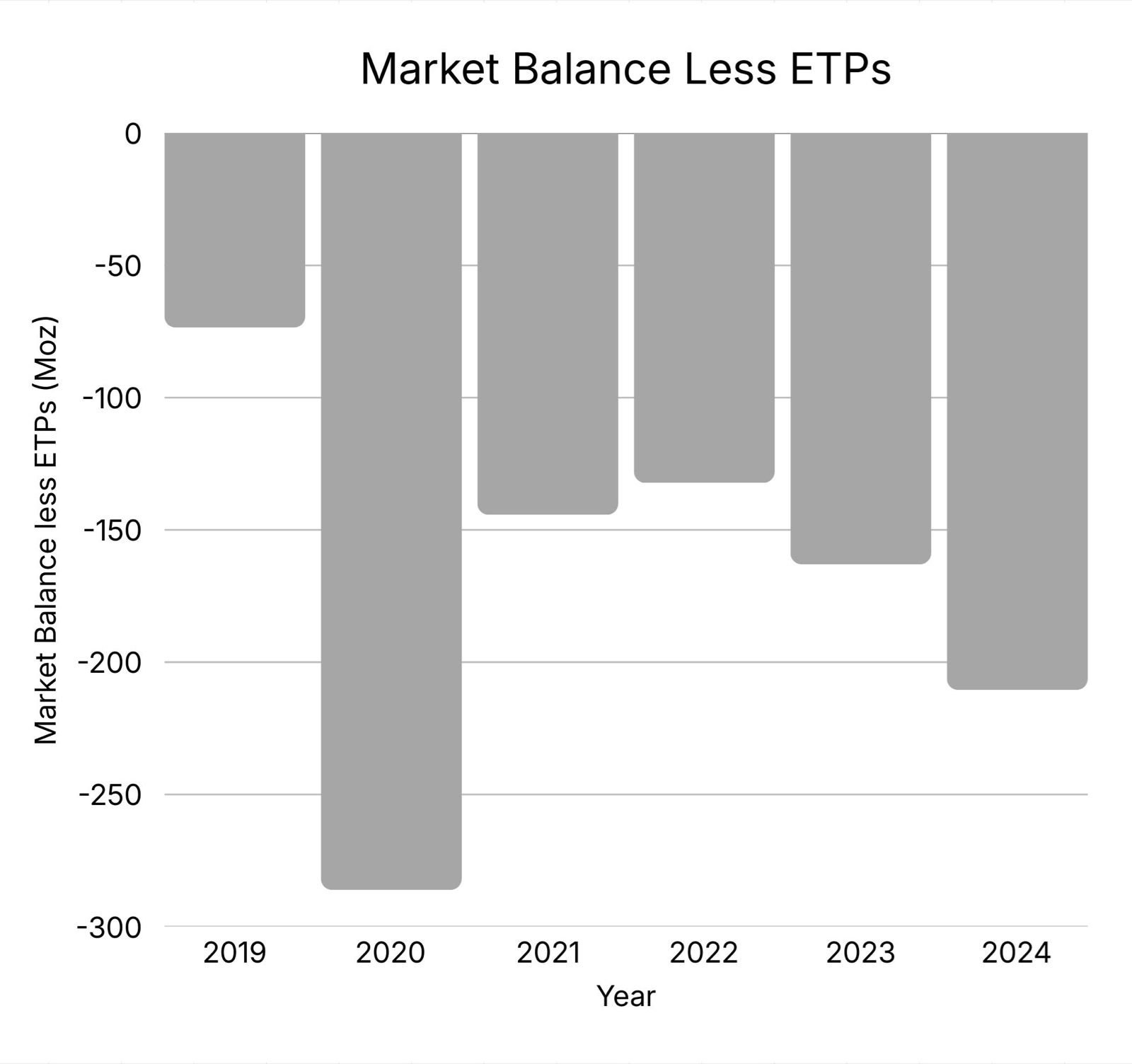

To truly comprehend the violence of the 2025 price action, one must look beneath the surface of daily charts to the fundamental geology and economics of the silver market. The market has been operating in a persistent, deepening structural deficit since 2019. According to data compiled from the Silver Institute and other industry analysts, the cumulative supply shortfall from 2019 through the end of 2025 has exceeded 1 billion ounces.[1]

This deficit is not a mere accounting abstraction; it represents a physical drawdown of above-ground stocks. For five consecutive years, the world has consumed significantly more silver than it has produced. In 2024 alone, the deficit was estimated at roughly 149 million ounces. While the 2025 deficit was projected to narrow slightly to roughly 95-117 million ounces, the cumulative effect of these consecutive shortfalls has been the draining of global vaults.[17]

The concept of "above-ground stocks" has historically been used by bearish analysts to argue that there is plenty of silver available to meet demand. However, the events of 2025 proved that much of this inventory is "sticky"—it is held by long-term investors, locked in ETFs, or utilized in industrial forms (like silverware or decorative items) that are not easily recyclable or mobilized. The "free float"—liquid silver available for immediate delivery to exchanges like the LBMA or COMEX—effectively evaporated in late 2025, leaving the market vulnerable to the price shocks we witnessed.

2.2 The Inelasticity of Mine Supply

A critical and often misunderstood factor driving this deficit is the extreme inelasticity of silver mine supply. Unlike gold, which is primarily mined for its own value, approximately 72% to 80% of global silver production comes as a byproduct of lead, zinc, copper, and gold mining.[1]

This geological reality has profound economic implications for the silver market:

•Price Insensitivity: Because silver is a secondary revenue stream for a copper or zinc miner, these companies do not ramp up production merely because silver prices rise. A massive copper mine in Chile or a zinc mine in Australia determines its production output based on the price of copper or zinc, not silver. Therefore, even if silver hits $100, these mines will not produce more unless the base metal markets also demand it.

•Development Lag Times: Even for primary silver miners (the remaining 20-28% of supply), the timeline from discovery to production is immense. New mining projects face rigorous permitting, environmental studies, and construction phases that can take 10 to 15 years. The severe lack of capital investment in the sector between 2011 and 2020 meant there was no pipeline of new projects ready to come online in 2025 to meet the demand surge.[2]

•Declining Ore Grades: Global mine production has remained essentially flat, hovering between 815 and 845 million ounces annually, despite the explosive price incentives.[1] Ore grades at major primary mines have deteriorated, meaning miners must move more tons of earth to recover the same amount of silver, increasing costs and capping output.

In 2025, global mine production was projected to remain stagnant at approximately 835 million ounces, a level wholly insufficient to cover even industrial demand, let alone the resurgence in investment buying.[2]

2.3 The Failure of Recycling to Fill the Gap

Historically, market analysts believed that high prices would elicit a flood of recycled silver (scrap) to balance the market. The theory was that as prices rose, grandmother's silverware and old jewelry would flood into refineries. While 2025 did see an uptick in recycling—particularly from silverware and jewelry as prices crossed the psychological $50 threshold—industrial recycling remains technically challenging and largely uneconomical.

Much of the silver used in modern electronics, smartphones, and solar panels is "thrifty" usage—microscopic amounts embedded in complex matrices of other materials. Recovering this silver is energy-intensive, environmentally hazardous, and expensive. While recycling rose by approximately 6% in 2024, reaching a 12-year high of roughly 194 million ounces, this increase was negligible compared to the widening industrial deficit.[20] The "scrap flood" that bears predicted would cap prices at $50 never materialized in sufficient volume to halt the rally, proving that modern industrial demand is largely dissipative—once the silver is used, it is often gone forever.

3. The Inventory Squeeze: The Disconnect Between Paper and Physical

The defining narrative of the 2025 silver market was the breakdown of the "Paper Market" (futures and derivatives) due to the exhaustion of the "Physical Market." This disconnect manifested visibly in the three major global vaults: COMEX (New York), LBMA (London), and the SGE/SHFE (Shanghai).

3.1 COMEX: The Emptying of New York

The COMEX (Commodity Exchange, Inc.) has traditionally been the primary venue for price discovery, despite dealing primarily in paper contracts where cash settlement is the norm. However, in 2025, market participants began standing for delivery in unprecedented numbers, breaking the implicit agreement that futures are for hedging, not sourcing metal.

Registered inventories—silver that is warranted and available for immediate delivery against futures contracts—plummeted. By late 2025, registered stocks had declined by approximately 70% from their 2020 peaks.[1] From a high of nearly 150 million ounces in the registered category, levels dropped toward the 30-40 million ounce range. This is a dangerously low buffer for an exchange that trades hundreds of millions of ounces in paper volume daily.

This physical stress resulted in a market condition known as "backwardation." In a healthy market, prices exist in "contango," where future delivery costs more than immediate delivery (reflecting storage, insurance, and interest costs). In Q4 2025, the silver curve inverted. Spot prices traded significantly higher than future months, a classic and urgent signal of physical scarcity.[1] Traders were willing to pay a premium to get their hands on metal now rather than wait, fearing that the metal might not be available in the future.

3.2 LBMA: The London Emergency and Lease Rate Spikes

London is the hub of the physical wholesale market, where the vast majority of the world's silver trades over-the-counter (OTC). In October 2025, the London market experienced a near-systemic failure. Lease rates—the interest rate paid to borrow physical silver—spiked violently. Short-term overnight lease rates annualized at over 100% at the peak of the squeeze, while one-month rates jumped to over 30%.[22]

This spike indicated a desperate scramble for physical bars. Bullion banks and industrial users who were short the metal (had sold it without owning it) needed to borrow it to meet delivery obligations, but there were no lenders. To solve this liquidity crisis, London was forced to import massive quantities of silver.

Data from October 2025 reveals a record inflow of 54 million ounces into London vaults.[22] Crucially, much of this metal was sourced from China and COMEX warehouses. This was not a sign of abundance, but of an emergency mobilization of global stocks to prevent a default in the London market. The system barely held together by shuffling metal across the Atlantic and from the Far East to plug the holes in London's balance sheet.

3.3 Shanghai: The Vacuum in the East

While London scrambled to find metal, Shanghai was being drained. The Shanghai Gold Exchange (SGE) and Shanghai Futures Exchange (SHFE) saw inventories collapse to decade lows, driven by the country's massive industrial engine.

•Record SGE Withdrawals: In October 2025 alone, a staggering 387 tonnes of silver were physically withdrawn from the SGE.[1] This represents industrial users taking possession of metal to ensure production continuity for solar panels and electronics.

•Inventory Levels: Combined inventory across Chinese exchanges fell to roughly 531 tonnes (531,211 kg) by late 2025, the lowest level since 2015.[26]

•The Shanghai Premium: Due to this scarcity, silver in Shanghai traded at a persistent premium to London and New York. This premium reached as high as 10-15% over international spot prices, creating a one-way valve: metal flowed into China for consumption, and only flowed out when prices were astronomically high or politically directed to ease Western squeezes.[9]

The dynamic in late 2025 was clear: China was consuming silver at a voracious rate for its solar and EV industries, depleting its domestic stocks and forcing it to compete aggressively for global supply, thereby setting the floor for global prices.

4. The Geopolitical Pivot: Silver as a Strategic Weapon

In 2025, silver graduated from being a mere commodity to a matter of national security. The geopolitical tensions between the United States and China began to manifest directly in the silver market, further tightening supply.

4.1 US Critical Mineral Designation

In late 2025, the United States Department of the Interior, through the U.S. Geological Survey (USGS), officially added silver to the Critical Minerals List.[28] This designation is reserved for minerals that are essential to the economic or national security of the U.S. and have a supply chain vulnerable to disruption.

This policy shift has massive implications for the market:

•Government Support: It opens the door for federal funding, tax incentives, and streamlined permitting for domestic silver mining projects, acknowledging that reliance on foreign silver is a strategic vulnerability.

•Stockpiling: It creates the legal framework for the US government to potentially build a strategic stockpile of silver for defense and energy needs, adding a new, price-insensitive buyer to the market.

•Supply Chain Security: It signals to US manufacturers (defense, aerospace, energy) that they must secure non-adversarial sources of silver, potentially bifurcating the global market into "Western" and "Eastern" supply chains.

4.2 China's Export Controls: The "Rare Earth" Playbook

Simultaneously, China moved to ring-fence its own silver supply. The Ministry of Commerce announced that effective January 1, 2026, silver exports would be subject to a strict licensing regime.[4]

Under the new rules:

•Quotas and Licenses: Only companies with specific licenses are permitted to export silver. The list of approved exporters was restricted to approximately 44 firms, primarily large state-owned enterprises.[4]

•Strategic Resource: Chinese state media and industry insiders began referring to silver as a "strategic resource," explicitly comparing the new controls to China's historical management of Rare Earth elements.[1]

•Impact: China is the world's third-largest silver producer and a major refiner. By restricting exports, Beijing is effectively prioritizing domestic industrial needs (solar panels, EVs) over the global market. This policy exacerbated the global shortage in Q4 2025, as Western buyers rushed to front-run the implementation of these rules.

The synchronization of these policies—US designation and Chinese restriction—confirmed that the world's superpowers now view silver not as a currency, but as a critical component of 21st-century technological supremacy.

5. Industrial Demand: The Unstoppable Engine

While investment demand creates volatility, industrial demand creates the price floor. In 2025, three sectors drove industrial consumption to record heights: Solar Photovoltaics (PV), Electric Vehicles (EVs), and Artificial Intelligence (AI).

5.1 The Solar Singularity: Technology Shifts

The solar industry remains the leviathan of silver consumption. In 2024 and 2025, the industry underwent a massive technological transition from PERC (Passivated Emitter and Rear Cell) technology to TOPCon (Tunnel Oxide Passivated Contact) and HJT (Heterojunction) cells.

Crucially, these newer, more efficient technologies require significantly more silver paste per watt of energy produced. TOPCon cells use approximately 50% more silver than PERC cells, and HJT cells use nearly double.[2]

•Thrifting Limits: For years, manufacturers successfully "thrifted" silver (used less per unit) to offset rising demand. However, 2025 highlighted the physical limits of this thrifting. To achieve higher efficiencies, more silver is required. The "Jevons Paradox" took effect: as solar energy became cheaper and more efficient due to these new cells, total demand for solar installations exploded, overwhelming the per-unit savings of thrifting.

•China's Dominance: China installed record gigawatts of solar capacity in 2025, driving the massive withdrawals from Shanghai vaults discussed earlier.

5.2 The Electrification of Transport

The EV revolution continued to act as a secondary engine of demand. An electric vehicle consumes up to 2-3 times more silver than an internal combustion engine (ICE) vehicle.[2] Silver is used heavily in the battery management systems, extensive cabling, and the myriad of electronic control units that govern modern EVs. With global EV penetration rising, particularly in China and Europe, the automotive sector's claim on annual silver supply continued to grow, shifting from a niche source of demand to a pillar of the market.

5.3 AI and the Compute Cycle

A nascent but rapidly growing source of demand in 2025 was the AI hardware boom. Data centers, high-performance computing chips, and 5G infrastructure all rely on silver's unmatched conductivity. As the "AI Arms Race" between the US and China intensified, demand for high-end connectors and semiconductor packaging—all containing silver—surged. While smaller in tonnage than solar, this demand is highly price-inelastic; a $100 increase in the price of silver is negligible for a $30,000 AI server rack, meaning this sector will continue to buy regardless of price.[2]

6. The "Gamma Squeeze" and Investment Flows

While fundamentals loaded the gun, the derivatives market pulled the trigger. The explosive rally in December 2025 was amplified by a "gamma squeeze" in the options market, centered on the iShares Silver Trust (SLV).

6.1 The Mechanics of the Gamma Squeeze

As silver prices began to rise in Q4, retail and institutional investors piled into call options on SLV.[36] Options dealers (Market Makers), who sell these calls, are inherently short the market. To hedge their risk, they must buy the underlying asset (SLV shares or silver futures) as the price rises—a process known as "delta hedging."

As the price accelerates, the "delta" of these options increases, forcing dealers to buy more silver to remain hedged. This creates a feedback loop: Buying drives prices up → Delta increases → Dealers buy more to hedge → Prices go up further. In December 2025, this loop went vertical. Market data indicates massive activity in SLV options, with speculators targeting deep out-of-the-money strikes that quickly became in-the-money.[36] This mechanical buying forced billions of dollars into the silver market in a matter of weeks, creating a vertical price ascent.

6.2 ETF Inflows: The Return of the Western Investor

After years of apathy and net outflows, Western investors returned to silver ETFs with a vengeance.

•SLV Inflows: The largest silver ETF, SLV, saw net inflows of approximately $2.3 billion in 2025.[1]

•Physical Trusts: Fully allocated trusts like Sprott Physical Silver Trust (PSLV) and Aberdeen (SIVR) also recorded hundreds of millions in inflows, removing large 1,000-ounce bars directly from the commercial market.[40]

This resurgence of Western investment demand clashed with the physical shortage in the East, creating the competition for ounces that drove lease rates and premiums to record highs.

7. The "Debasement Trade": Monetary Context

The silver rally did not occur in a vacuum. It was part of a broader "debasement trade"—a global move into hard assets to protect against currency inflation and fiscal profligacy.

7.1 The Dollar and Debt

Throughout 2025, concerns regarding US fiscal sustainability mounted. With the US debt-to-GDP ratio climbing and interest expensed on debt consuming a larger portion of the federal budget, the market began to price in a long-term devaluation of the US dollar.[1] Investors viewed silver not just as an industrial commodity, but as an "inflation-proof" monetary asset. The correlation between silver and real interest rates, which had broken down in previous years, reasserted itself. Expectations of Federal Reserve rate cuts in 2026 further fueled the fire, as lower yields reduce the opportunity cost of holding non-yielding assets like gold and silver.[43]

7.2 Central Bank Diversification

While Central Banks primarily buy gold, their aggressive accumulation of precious metals in 2025 signaled a broader move away from fiat reserves. The People's Bank of China (PBoC) and the Reserve Bank of India (RBI) were notable buyers of gold, creating a "halo effect" that lifted silver. Furthermore, reports surfaced of Russia accumulating silver reserves, a rare move that hinted at the potential remonetization of the white metal in the BRICS bloc.[45]

8. Conclusion: The New Reality at $50

The 2025 silver market was defined by the collision of unstoppable force (industrial demand) and immovable object (inelastic supply). The Christmas Rally to $84 was the market's first attempt to find a price that would equilibrate this imbalance. While the subsequent crash to ~$70 was painful for late entrants, it did not alter the fundamental reality.

Key Takeaways

•The Floor has Moved: The days of $20 or $30 silver are likely over. The structural inputs—mining costs, solar demand, and physical scarcity—suggest that $50 is the new valuation floor for 2026.[1]

•Volatility is the Norm: Silver is a small, illiquid market compared to gold. The violence of the Christmas Rally and Crash demonstrates that volatility is a feature, not a bug. Investors must be prepared for 10-20% swings in both directions.

•Physical Matters: The disconnect between paper and physical markets means that owning physical metal (or fully allocated trusts) is safer than holding leveraged paper contracts, which are subject to margin hikes and regulatory intervention.

•The Squeeze is Structural: The deficits are cumulative. The billion ounces lost since 2019 cannot be replaced quickly. As long as the green energy transition accelerates, the squeeze on silver inventories will persist.[47]

9. 2026 Outlook: What to Watch

As we enter 2026, the market remains in a precarious state of balance. The following indicators will determine the next major move:

9.1 Price Targets and Support

•Bear Case: A technical pullback could retest the breakout levels at $50-$54. If industrial demand softens due to a global recession, prices could consolidate in this range.[5]

•Base Case: Most analysts see silver stabilizing between $60 and $75, digesting the massive gains of 2025.

•Bull Case: With the gold-to-silver ratio still elevated historically (57:1 vs historical 15:1), and industrial shortages intensifying, banks like Citi have issued targets as high as $110 per ounce for late 2026.[43]

9.2 The Watchlist for Retail Investors

•SGE Withdrawals: Monitor the monthly withdrawal data from Shanghai. If China continues to drain 300+ tonnes a month, Western markets will break again.

•COMEX Registered Stocks: Watch if inventories stabilize or continue to bleed. A drop below 30 million ounces in registered stocks would signal a critical emergency.

•ETF Flows: Sustained inflows into SLV and PSLV act as a vacuum for commercial bars. If 2026 sees continued retail buying, the price must rise to ration demand.

•China's Export Policy: Implementation of the Jan 1, 2026 export controls. Any signs of strict enforcement or reduced quotas will send shockwaves through the supply chain.[4]

Final Verdict

The "Christmas Rally" of 2025 was a warning shot. It demonstrated that the physical silver market is running on fumes. For the strategic investor, the repricing of silver is not a completed event, but an ongoing process of realization that the world's most indispensable industrial metal is running out.

(Note to Reader: This report aggregates data from the Silver Institute, COMEX, LBMA, and SGE reports as of year-end 2025. All financial investments carry risk, and silver is historically one of the most volatile asset classes.)

Works Cited

Silver Analysis 2025 DRAFT.docx

Silver Supply Deficit: 5-Year Shortage Reaches 800M Ounces, Discovery Alert, accessed January 5, 2026

China to Restrict Silver Shipments Starting New Year, Trading Economics, accessed January 5, 2026

China's Exclusive Export List for Critical Metals (2026-2027): Who's In and Why It Matters, Rare Earth Exchanges, accessed January 5, 2026

Silver 2026 outlook: The trade to watch, FOREX.com, accessed January 5, 2026

Hi Ho Silver Away! Silver Breaks $80 as Poor Man's Gold Explodes, MarketBeat, accessed January 5, 2026

Gold and Silver Outlook 2026: Can the Frenzy Continue?, NAI 500, accessed January 5, 2026

S&P 500 Snapshot: Index Posts 16.4% Gain in 2025, Advisor Perspectives, accessed January 5, 2026

Silver and Platinum Surge as Chinese Price Premiums Gap Up, SD Bullion, accessed January 5, 2026

Peter Krauth: Silver Prices Could Reach $125 in 2026, NAI 500, accessed January 5, 2026

Silver price hits $70 per ounce as historic rally accelerates, The Economic Times, accessed January 5, 2026

Silver slides on New Year's Eve after a record rally in 2025, Seeking Alpha, accessed January 5, 2026

Gold and Silver Prices Plunged Monday After Last Week's Big Rally. Here's Why., Investopedia, accessed January 5, 2026

Why Silver Is Falling With Gold and Why Robert Kiyosaki Predicts a $200 Price by 2026, Finance Magnates, accessed January 5, 2026

Gold Sinks $200, Silver -14% from China's Christmas Chaos, BullionVault, accessed January 5, 2026

Real Silver Squeeze: Industrial Demand Drives Triple-Digit Price Potential, Discovery Alert, accessed January 5, 2026

The Silver Market is on Course for Fifth Successive Structural Market Deficit, The Silver Institute, accessed January 5, 2026

Market Balance Silver Supply and Demand, Money Metals, accessed January 5, 2026

SILVER SUPPLY & DEMAND, The Silver Institute, accessed January 5, 2026

Silver Industrial Demand Reached a Record 680.5 Moz in 2024, The Silver Institute, accessed January 5, 2026

Silver Supply Tightness 2025: Why Record Prices Reflect Seven Years of Structural Deficits, Bullion Trading LLC, accessed January 5, 2026

London Bullion Vaults Silver Inflows Surge to Historic 54 Million Ounces, Discovery Alert, accessed January 5, 2026

Silver Soars to Unprecedented Highs, Shattering 45-Year Record, NAI 500, accessed January 5, 2026

After stellar 2025 rally, gold and silver may extend gains in 2026, Gulf Today, accessed January 5, 2026

Silver's Split-Screen: Record Shanghai Withdrawals, 10-Year Low Vaults, InProved, accessed January 5, 2026

Silver Rockets To $57 Record — Shanghai Inventories Hit 10-Year Low, USAGOLD, accessed January 5, 2026

Chinese Silver stocks hit 10-year low – ING, Octa, accessed January 5, 2026

Silver Added to USGS 2025 List of Critical Minerals, Apollo Silver, accessed January 5, 2026

Critical Update! USGS Expands Mineral List, Brownstein, accessed January 5, 2026

Final 2025 List of Critical Minerals, Federal Register, accessed January 5, 2026

China Silver Export Restrictions Transform Global Market Dynamics, Discovery Alert, accessed January 5, 2026

China has announced restrictions on silver exports from 2026, ICICIdirect, accessed January 5, 2026

China's Silver Export Ban Sparks $84 Rally!, WhalesBook, accessed January 5, 2026

+$50 per oz Silver as London Lease Rates Signal Short Squeeze, SD Bullion, accessed January 5, 2026

Silver Investment Outlook Mid-Year 2025, Sprott, accessed January 5, 2026

Ishares Silver Trust Trade Ideas, TradingView, accessed January 5, 2026

The Great Silver Gamma Squeeze, SpotGamma, accessed January 5, 2026

Betting on the 'Santa Squeeze': Unusual Options Activity Surges, Financial Content, accessed January 5, 2026

Gold Left Behind as Silver Hikes 132% YTD: The ETF Playbook for 2026, Finviz, accessed January 5, 2026

Sprott Physical Gold and Silver Trust, Sprott, accessed January 5, 2026

Silver Outshines Gold, AI: ETFs Power A Hot 2026 Diversification Play, Webull, accessed January 5, 2026

Gold and Silver Shatter Records as 2026 Opens to a "Perfect Storm" of Economic Anxiety, Financial Content, accessed January 5, 2026

Gold and Silver Price Forecast 2026: Why Precious Metals Hit Record Highs, Kavout, accessed January 5, 2026

Why gold, silver, and copper are all surging together, The Economic Times, accessed January 5, 2026

Silver Price Predictions 2026: After a 120% Surge, What's Next?, GoldSilver, accessed January 5, 2026

Gold and Silver Outlook for 2026: Why Hard Assets May Beat Stocks, FXEmpire, accessed January 5, 2026

Silver Price Hits $64 as Supply Deficit Enters Fifth Year, Prices May Reach $100/Oz, Carbon Credits, accessed January 5, 2026